Quarterly Economic Newsletter – Q2, 2026

Summary

The U.S. economy continues to grow at a moderate pace, with low unemployment but persistent inflation keeping interest rates elevated. Washington’s economy is generally keeping pace with national trends, while Oregon, particularly the Portland area, has faced job losses and slower growth. The biggest risk to the economic outlook is the conflict in Iran, which could drive up energy prices and potentially lead to a recession.

The United States economy is growing moderately well, with Washington keeping pace with the nation but Oregon stumbling. The future, though, is unusually uncertain given the Iran War’s impact on oil prices. This constitutes a major risk of recession, which would impact the Pacific Northwest as well as the U.S. economy.

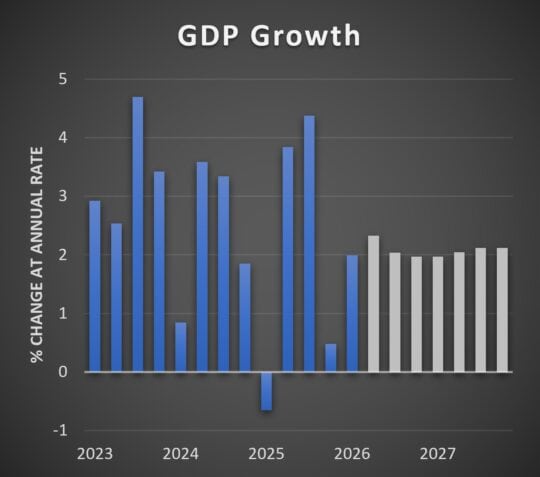

Our broadest measure of the national economy, gross domestic product adjusted for inflation, grew by two percent in the first quarter. The long-run average has been three percent, of which two percentage points came from productivity growth (more output per hour worked) and one percentage point from labor growth. But now our native-born labor force of working age is hardly growing. In recent years immigration propped up total labor supply, but new policies have ended most immigration. As a result, our two percent GDP growth constitutes our full potential.

A number of high-profile companies have announced layoffs, but the hard data on actual terminations show little change. The national unemployment rate remains low at 4.3 percent, though above the rate of a few years ago when employers found few people available to hire.

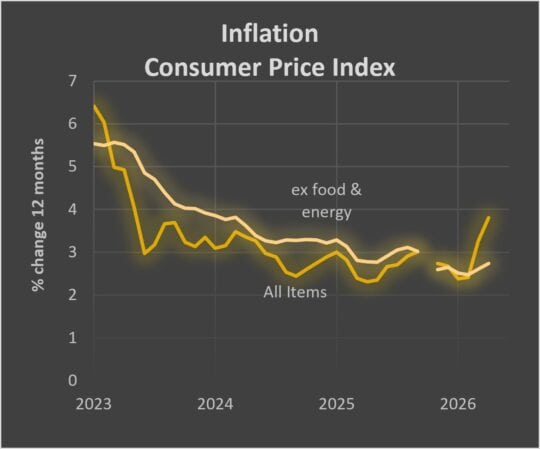

Inflation remains a problem, with the latest Consumer Price Index rising 3.8 percent. A good bit of that jump was due to gasoline, with some effect from tariffs. Stripping these out, though, still leaves inflation above the Federal Reserve’s two-percent target.

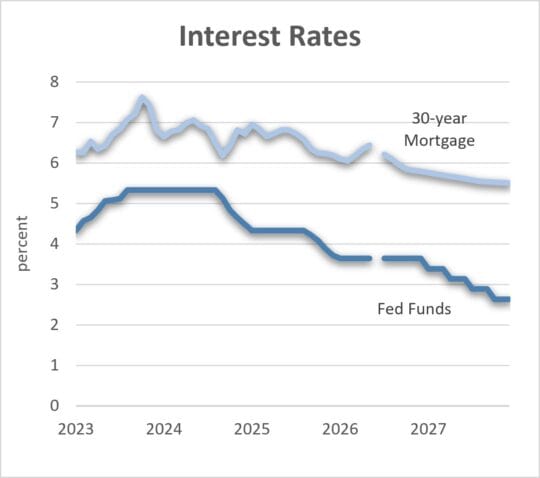

Looking at our domestic data, the Federal Reserve has little reason to cut interest rates, as was generally expected early in the year. Decent employment and high inflation have led to market expectations that the Fed will leave rates unchanged this year. And if they make a move, it will more likely be to raise rates than to cut them.

The war in Iran throws a monkey wrench into the economic forecast, however. The Strait of Hormuz is the path for 20 percent of the world’s oil production, which amounts to about eight percent of total energy production. If the Strait remains closed for months, the world will have to cut its energy consumption. That adjustment involves consumers cutting back on both energy and discretionary purchases. Some companies that had been profitable will lose money and cut staff.

The United States is a net exporter of oil, but producers sell to whoever pays the highest price. American consumers and businesses will not be exempt from the pain.

If the war triggers a recession, that downturn will probably be about half as bad as the 2008-09 recession. It will cause widespread economic pain, but it won’t be the worst we’ve seen in the past decades. (The forecast charts assume the Strait is soon re-opened.)

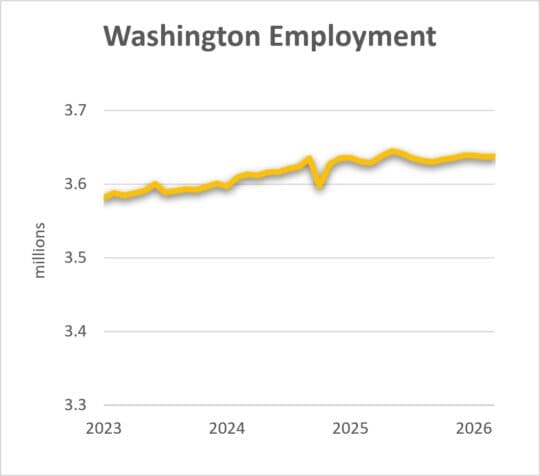

Washington matches the national pattern of level employment. That’s a bit troubling because its population is growing faster than the country as a whole. Thus, the economy is underperforming its potential by a little. Unemployment is somewhat elevated relative to the nation. Looking forward, migration will likely slow. If the national economy avoids a recession, employment in the state will improve somewhat. But a global recession would certainly impact Washington State.

The Puget Sound region shed jobs, while rural counties gained them, a dramatic reversal of the usual pattern. Absent a recession, look for Puget Sound to rebound. But in the case of a recession hitting the country, all parts of the state would likely suffer.

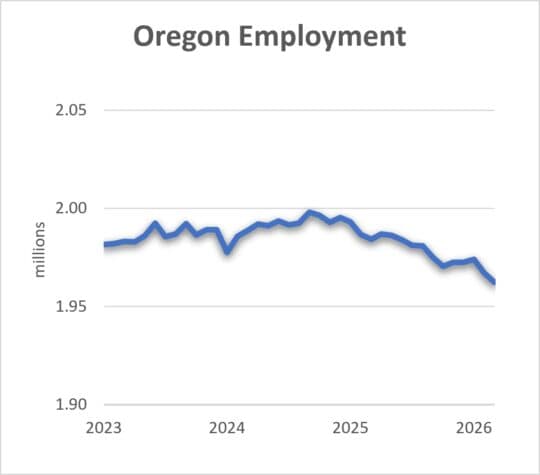

Oregon has lost jobs over the past 12 months, for a drop of over a full percentage point. The Portland area is the greatest problem. Its three largest counties dropped 14,000 jobs in the past 12 months. Other parts of the state had ups and downs, but in the aggregate added 2,000 jobs. Population data also shows more people have moved out of the Portland area than moved in over the past five years. The rest of the state had a small net increase from migration.

Oregon would definitely feel a national recession. If the national economy remains stable, Portland’s economic future will partly depend on the fortunes of its major employers. But high taxes and restrictive economic policies will continue to slow economic recovery. The rest of the state, however, should proceed with light growth in economic activity, consistent with its population growth.

The economic outlook for the nation and the region would be stable but for the risks coming from the Persian Gulf.