Quarterly Economic Newsletter – Q1, 2026

Summary

The Iran war raises recession risks by disrupting oil supply, threatening U.S. growth. Washington and Oregon show flat employment and slower housing growth, with population trends diverging; prolonged conflict could worsen regional conditions, while a quick resolution would restore moderate growth.

The war in Iran complicates the economic outlook. The downside risk is significant: a global recession. A quick end would bring us back to the old forecast—from a month ago—of stable economic growth in the United States and the Pacific Northwest. Although the future is never certain, it’s not always this uncertain.

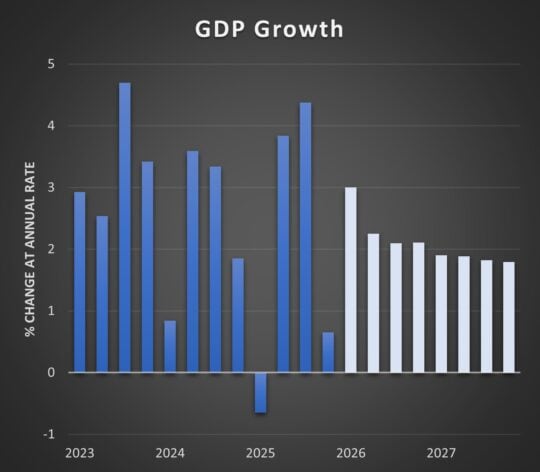

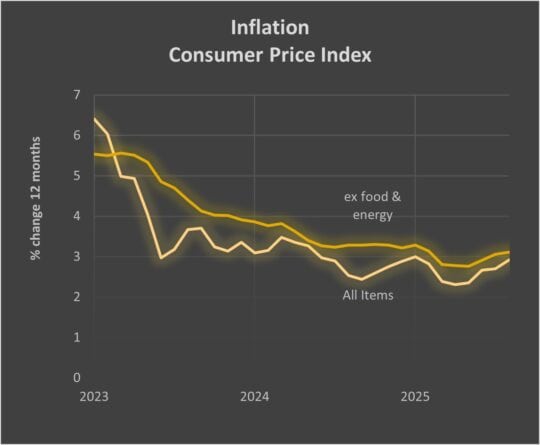

Prior to the war, the U.S. economic outlook was stable. Growth of gross domestic product was a little light in the fourth quarter of 2025, due partially to the government shutdown, with rebound likely in the first quarter of 2026. Thereafter we would have moderate growth, with demand fueled by consumers and supported by business spending on equipment. Inflation was running hotter than the Federal Reserve’s target. Employment had been flat, but didn’t have much room to grow without immigrants adding to the labor force. Forecasters expected the Fed to cut short-term interest rates by a small amount in 2026.

With the Iran war, we must consider the effective closure of the Strait of Hormuz. Through it flows 20 percent of the world’s oil, which is six to seven percent of global energy usage. Continued closure of the Strait would be harsh. Rough estimates based on a year-long closure of the Strait show global GDP dropping a couple of percentage points. That would constitute a recession.

Economic growth trends highlighted in the Q1 2026 newsletter from Bank of the Pacific, emphasizing regional financial stability.The United States would feel that downturn even though we are net exporters of petroleum. American consumers and businesses must pay the world price, or else producers will ship the product overseas. Although long-run supply is elastic, in the short run there are limited options. Consumers faced with higher gasoline prices will spend less on discretionary purchases, and businesses may have to lay off workers who make those goods and services.

If the Iran war ends quickly, we return to the old forecast: steady economic growth, inflation coming down very slowly, and interest rates stable through 2026 and then edging down next year.

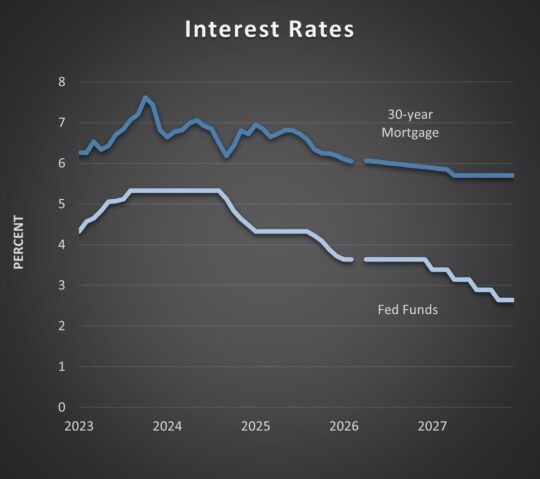

The Fed will likely ignore the spike in oil prices when adjusting short-term interest rates, just as they try to ignore tariff-induced price hikes. The calculations are difficult, so errors in monetary policy are more likely—in either direction. Short-term interest rates will be left unchanged this year, even with a new chair of the Federal Reserve Board. Long-term interest rates, such as on mortgages, have room to drop a little, but less than half a percentage point.

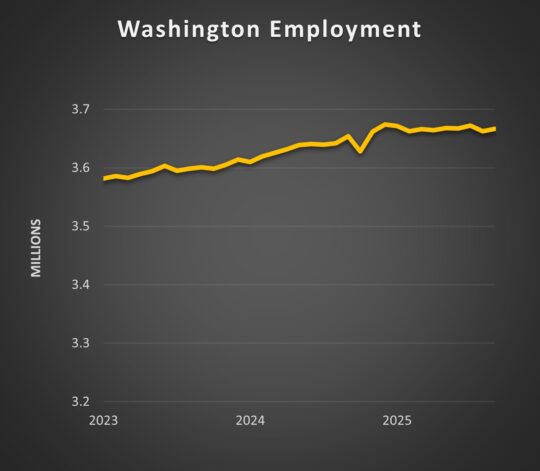

Employment in Washington was roughly level last year. We do not yet have any state level data for 2026. Gains were chalked up in healthcare—a national trend—offset by losses in government, construction and manufacturing. Although tech layoff announcements made the news, they have not yet shown up in the official statistics.

Home prices in the state rose by less than three percent, a far cry from a few years ago. Construction of new housing, both single family homes and apartment units, dropped last year. Soft construction is consistent with the flat economy. However, people continue to move into the state. Washington ranked 7th of the 50 states in population growth last year. This presents a challenge if employment does not grow in the coming years. However, population growth in Washington enables future job growth, and the state will likely rebound in 2026 and 2027.

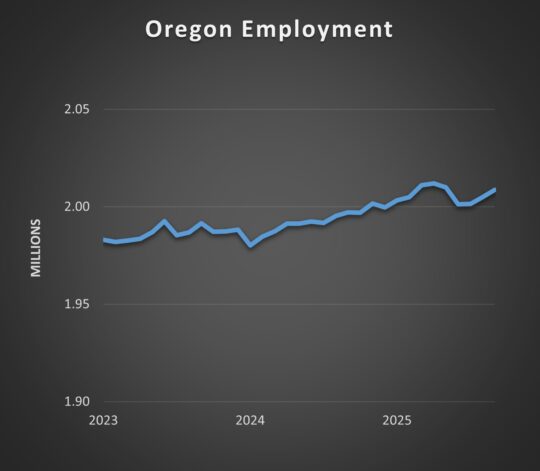

Oregon, like Washington, has seen hardly any employment gain in the past year. Jobs did increase in healthcare as well as leisure/hospitality, though manufacturing and construction declined. Two major private sector employers in the Portland area, Intel and Nike, have laid off workers. Population growth has been very light, in contrast with the state’s long history as a magnet for people looking for a change in scenery.

Home prices rose by two percent last year, in line with national appreciation. Apartment construction increased while single family homebuilding declined a little, netting out to a small increase. The number of housing units permitted actually exceeded the change in population, which helps housing affordability and should boost the state’s economic prospects in the coming year. However, Oregon’s high taxes and still-high housing costs make any turnaround slow to come.

Business strategy in this economic environment is quite difficult. So long as the war continues, delaying major commitments makes sense. When the Strait of Hormuz is safe for oil tankers, then the global and American economies will perform moderately well.